How to Navigate Financial Divorce Tips Successfully

Our Blog

How to Navigate Financial Divorce Tips Successfully

Divorce splits more than just your life-it splits your finances. The decisions you make about assets, taxes, and retirement accounts during this process will shape your financial health for decades.

We at Harnage Law PLLC help clients in Melbourne, Florida understand the financial divorce tips that protect their interests. This guide walks you through asset division, settlement strategies, and the tax consequences you need to know.

What Counts as Marital Property in Your Divorce

Marital vs. Nonmarital Property in Florida

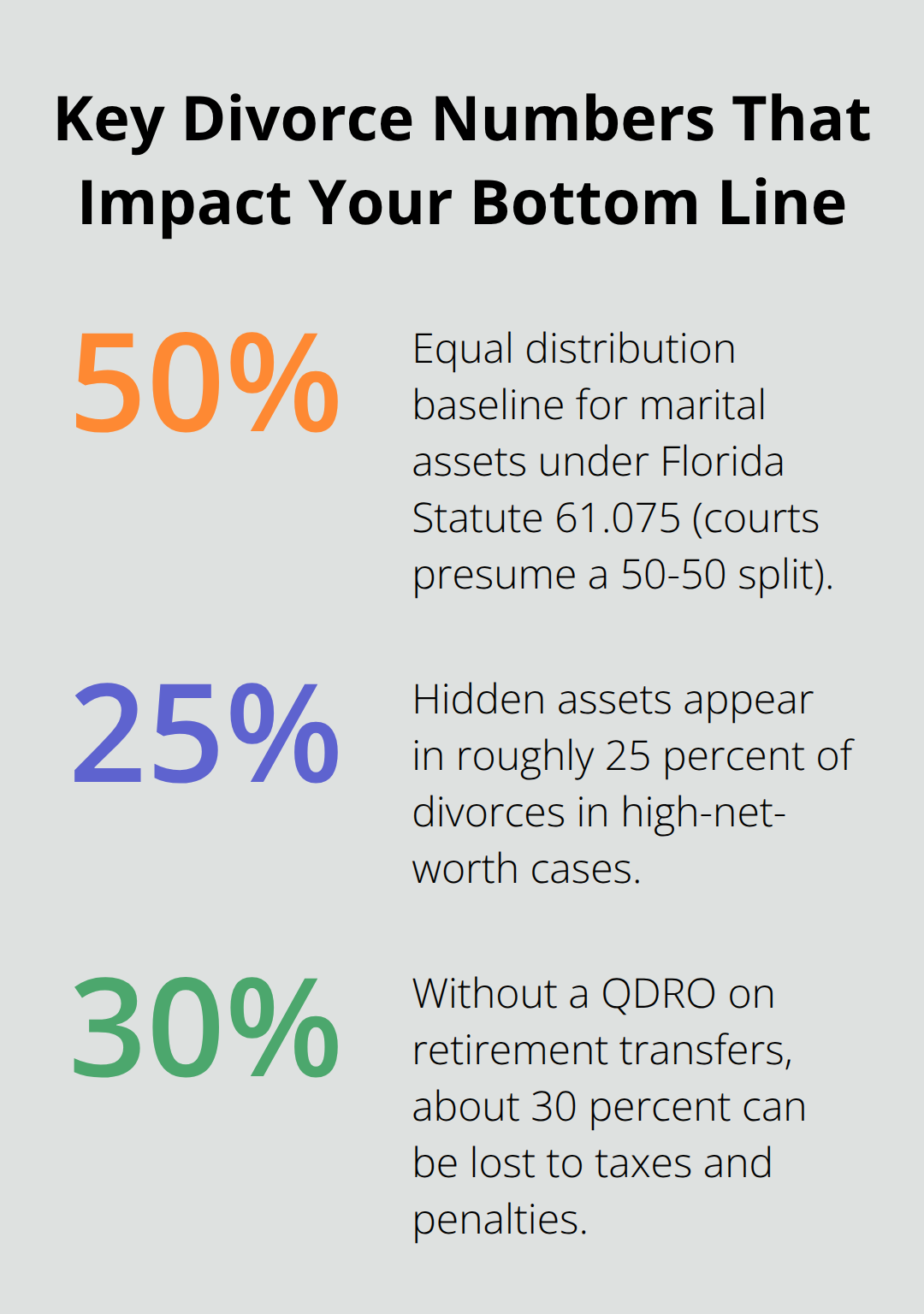

Florida law divides divorce assets into two categories: marital and nonmarital property. Marital property includes everything acquired during the marriage, regardless of whose name appears on the title. A home purchased jointly, a car titled to one spouse, retirement accounts funded during the marriage, and business interests developed while married all qualify as marital. Nonmarital property includes assets you owned before the marriage, inheritances, gifts from third parties, and assets acquired after separation. The distinction matters enormously because Florida Statute 61.075 starts with an equal distribution baseline for marital assets, meaning the court presumes a 50-50 split unless you prove factors that justify an unequal division.

The cut-off date for classification is typically the filing date of the divorce petition, though it can shift if you signed a valid separation agreement earlier. This timing directly affects what the court treats as marital versus separate property.

Title Ownership Does Not Determine Property Status

Many people assume that keeping an asset titled in one name keeps it nonmarital, but that assumption costs them thousands. A home purchased during the marriage with joint income becomes marital property even if only one spouse’s name appears on the deed. Courts look at when you acquired the asset and how you funded it, not simply who holds title.

Commingling funds accelerates this problem significantly. Depositing an inheritance into a joint account converts it from nonmarital to marital unless you can trace and prove the separate source, which courts require with clear and convincing evidence according to cases like Amato v. Amato and Archer v. Archer. Keep inheritances and gifts in separate accounts to preserve their nonmarital status.

Identifying Hidden Assets Before Settlement

Hidden assets appear in roughly 25 percent of divorces, according to financial professionals handling high-net-worth cases. Spouses conceal income through unreported cash businesses, delay bonus payments until after the divorce, shift funds to relatives, or create secret accounts. The discovery process in Florida requires both parties to exchange financial information within specific timeframes under the Florida Family Law Rules of Procedure, but gaps still emerge.

Request three years of tax returns, bank statements from every account, retirement plan statements, business tax returns if self-employed, and credit card statements to identify spending patterns that suggest hidden accounts. Pay attention to unexplained transfers, unusual wire activity, or accounts that suddenly close. Forensic accountants cost between $3,000 and $10,000 but recover substantially more in contested cases.

Gather your own financial documentation before filing to understand what exists, then compare it against what your spouse discloses. If your spouse transferred $50,000 to a family member’s account weeks before filing, that dissipation of marital assets can affect the final distribution under Florida Statute 61.075, which allows courts to consider assets wasted within two years before filing. This discovery phase sets the foundation for the settlement negotiations that follow.

How to Structure Your Asset Split in Melbourne, Florida

Document Everything Before Negotiation Begins

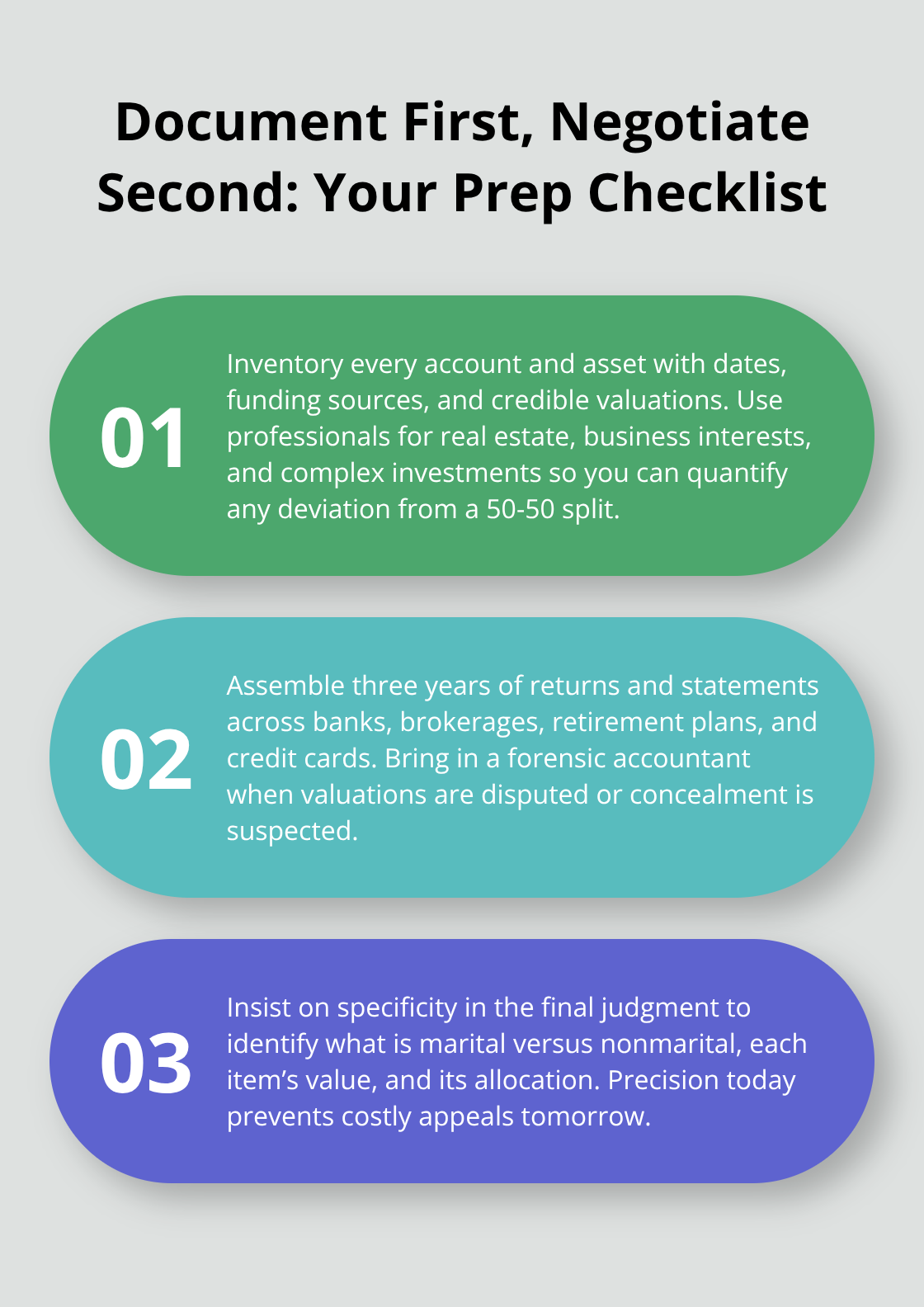

Reaching a fair settlement on asset division requires you to understand your negotiating position before you sit down at the table. Start by documenting every asset’s acquisition date, funding source, and current value with professional appraisals where needed. Courts in Florida apply Florida Statute 61.075, which presumes an equal 50-50 split of marital property unless factors like marriage length, each spouse’s contributions to homemaking or career sacrifices, or economic circumstances justify an unequal division. You need concrete numbers to argue any deviation from equal distribution.

Gather three years of tax returns, recent bank and investment statements, retirement account valuations as of the filing date, and professional appraisals for real estate or business interests. A forensic accountant costs $3,000 to $10,000 but becomes invaluable when the other side contests valuations or you suspect asset concealment. Do not accept rough estimates or promises to handle details later; the final judgment must include explicit findings identifying which assets are marital versus nonmarital, their individual valuations, and how each is allocated. Courts rarely modify these findings after judgment, so precision now prevents costly appeals later.

How Prenuptial and Postnuptial Agreements Change Your Strategy

Prenuptial and postnuptial agreements function as a shortcut around the statutory distribution framework, but only if they are valid and properly executed. Florida recognizes these agreements when both parties signed voluntarily with full financial disclosure and no fraud, coercion, or unconscionable terms. If you have a prenuptial agreement, obtain a copy immediately and have it reviewed because it may exclude certain assets from judicial distribution entirely, fundamentally changing your negotiation strategy.

Mediation Versus Litigation: When Each Makes Sense

Without a written agreement, mediation typically resolves 70 to 80 percent of family law disputes faster and cheaper than litigation. Mediation costs $1,500 to $5,000 total, while a contested trial can exceed $50,000 in attorney fees alone. Mediation also keeps sensitive financial details private, whereas trial records become public documents accessible at the courthouse.

However, mediation fails when one spouse refuses to disclose hidden assets or demands unreasonable terms. In those cases, litigation forces full discovery and allows a judge to impose a distribution the other side cannot block. Start with mediation if both parties appear willing to negotiate in good faith, but do not hesitate to pursue litigation if your spouse stonewalls or the financial gap between settlement offers remains substantial after several mediation sessions. The tax consequences of your chosen settlement path deserve equal attention, as different asset divisions carry vastly different long-term financial impacts.

Protecting Your Assets From Taxes During and After Divorce

How Cost Basis Affects Your Settlement Negotiations

Transferring assets to your spouse during divorce typically avoids immediate capital gains taxes under Section 1041 of the Internal Revenue Code, but this tax-free exchange creates a hidden liability that surfaces years later when you sell. If you receive investment property worth $300,000 with a cost basis of $100,000, the transfer itself generates no tax bill. However, when you eventually sell that property for $350,000, you owe capital gains tax on $250,000 in appreciation, not just the $50,000 gain since the divorce. The cost basis does not step up at divorce; you inherit your ex-spouse’s original purchase price.

This means your settlement negotiation must account for the future tax hit embedded in appreciated assets. Request a detailed cost basis analysis for every property, investment, and business interest before accepting any settlement offer. If your spouse insists on keeping the investment portfolio while you take the house, you need to know whether those investments carry substantial unrealized gains that will trigger thousands in taxes when sold. Undervaluing this tax consequence during settlement negotiations is one of the most expensive mistakes people make in divorce.

QDROs and Retirement Account Transfers

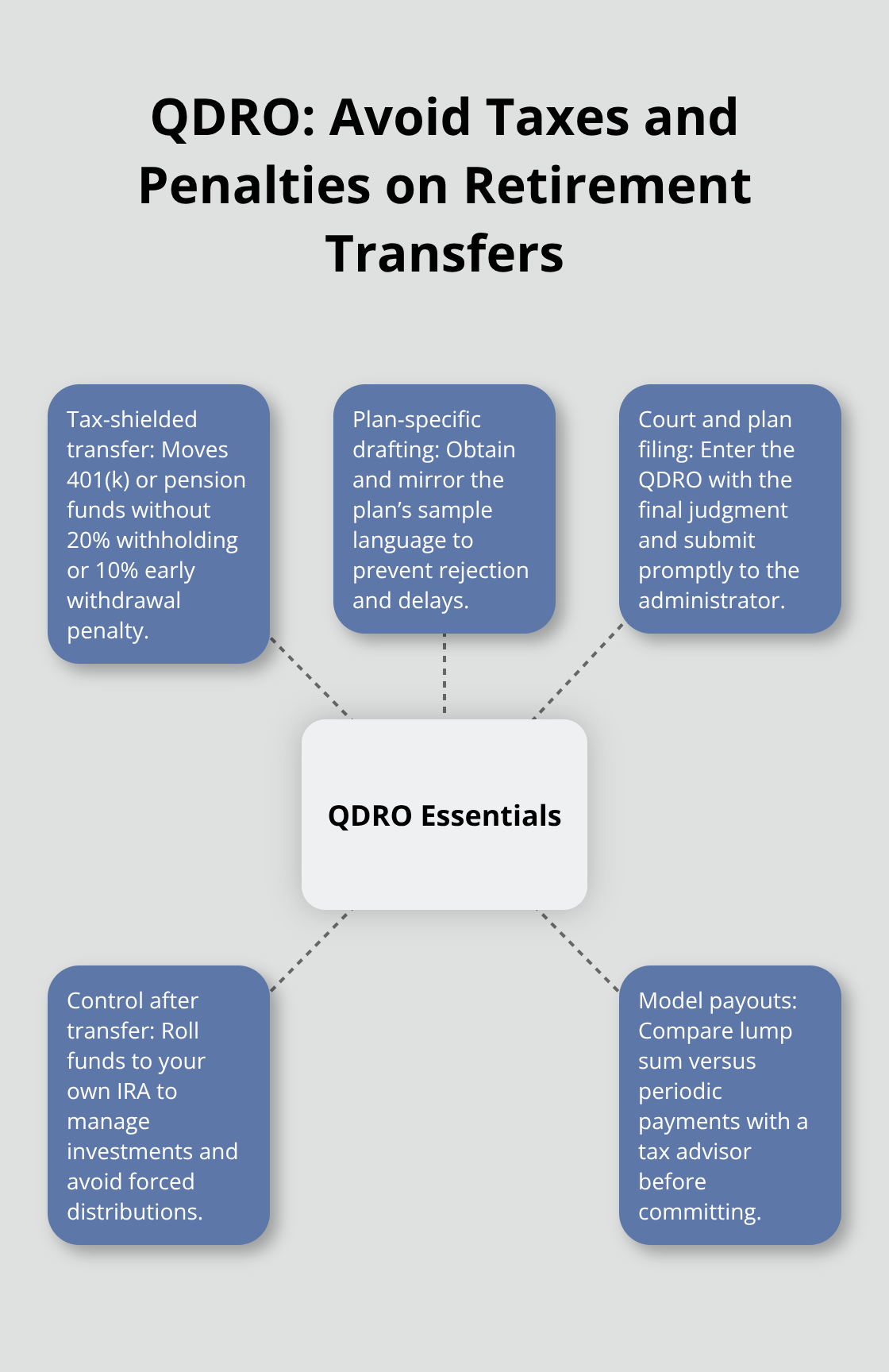

Retirement accounts demand separate attention because they require a Qualified Domestic Relations Order, or QDRO, to transfer without immediate tax penalties. A QDRO is a court order that allows one spouse to receive a portion of the other’s 401(k), pension, or similar plan without the 20 percent withholding tax and 10 percent early withdrawal penalty that normally apply. Without a QDRO, the transfer counts as a taxable distribution, and you lose roughly 30 percent to taxes and penalties immediately.

The QDRO must match the specific plan’s requirements precisely, and many attorneys draft them incorrectly, creating delays or rejection by the plan administrator. Request a sample QDRO from your spouse’s plan before finalizing your settlement to confirm the exact language needed. File the QDRO with the court as part of your final judgment, then submit it to the plan administrator immediately after the judge signs.

Do not assume the other side will handle this; treat it as your responsibility to ensure proper execution. After the transfer completes, consider rolling the funds into your own IRA to maintain investment control and avoid forced distributions at the plan’s timeline. The decision between a lump-sum distribution and ongoing payments from a pension carries different tax consequences, and a tax advisor should model both scenarios before you commit to either option.

Adjusting to Single-Filer Tax Status

Rebuilding your financial life after divorce requires a deliberate plan that acknowledges your changed household income and tax filing status. You transition from filing jointly to filing as a single filer, which pushes you into higher tax brackets on the same income. If you earned $75,000 while married filing jointly and your spouse earned $75,000, your combined income was $150,000 across two returns. Post-divorce, that $75,000 is now your entire household income on a single return, placing you in a materially higher effective tax rate.

Budget for increased tax liability immediately. Set aside 15 to 20 percent of your income for federal and state taxes rather than the 12 to 15 percent you may have withheld while married. Update your W-4 form with your employer within 30 days of the final judgment to adjust withholding. Simultaneously, update beneficiary designations on life insurance policies, retirement accounts, annuities, and any trusts to remove your ex-spouse or name new beneficiaries. Courts do not automatically remove ex-spouses from these designations, and failing to update them means your ex inherits thousands or more if you die before making changes.

Planning Your Post-Divorce Financial Strategy

Meet with a tax professional within 90 days of your divorce becoming final to review your asset allocation and investment strategy in light of your new financial situation. The portfolio that worked for a two-income household may not suit a single-income household, and rebalancing now prevents years of suboptimal returns.

Final Thoughts

Your divorce settlement does not end when the judge signs the order. The financial decisions you made during asset division, tax planning, and retirement account transfers will compound over the next 20 to 30 years, making the quality of your financial divorce tips and execution far more important than speed. Many people rush through settlement to end the emotional strain, then spend years recovering from tax mistakes or overlooked asset valuations that cost tens of thousands in lost wealth.

The foundation for protecting your financial interests starts before you negotiate. You must document every asset with acquisition dates and funding sources, obtain professional appraisals for significant property, and request cost basis analysis for appreciated investments. A seemingly equal 50-50 split can be financially unequal if one spouse receives assets with substantial unrealized capital gains while the other receives cash or low-basis property, so you need to understand the tax consequences embedded in each asset before you accept any settlement offer.

We at Harnage Law PLLC represent clients throughout Melbourne, Florida in complex family law matters where asset division and financial planning determine long-term outcomes. Contact Harnage Law PLLC to discuss how we can protect your financial interests and guide you toward a settlement that serves your future.