Divorce settlement Melbourne Florida: Reaching a Fair Agreement

Our Blog

Divorce settlement Melbourne Florida: Reaching a Fair Agreement

Divorce settlement negotiations in Melbourne, Florida require clear thinking and solid planning. The difference between a fair agreement and a costly mistake often comes down to understanding Florida’s laws and knowing what to protect.

At Harnage Law PLLC, we help clients navigate these decisions with practical guidance grounded in real-world experience. This guide walks you through the settlement process step by step.

What Makes a Settlement Fair in Florida Divorce

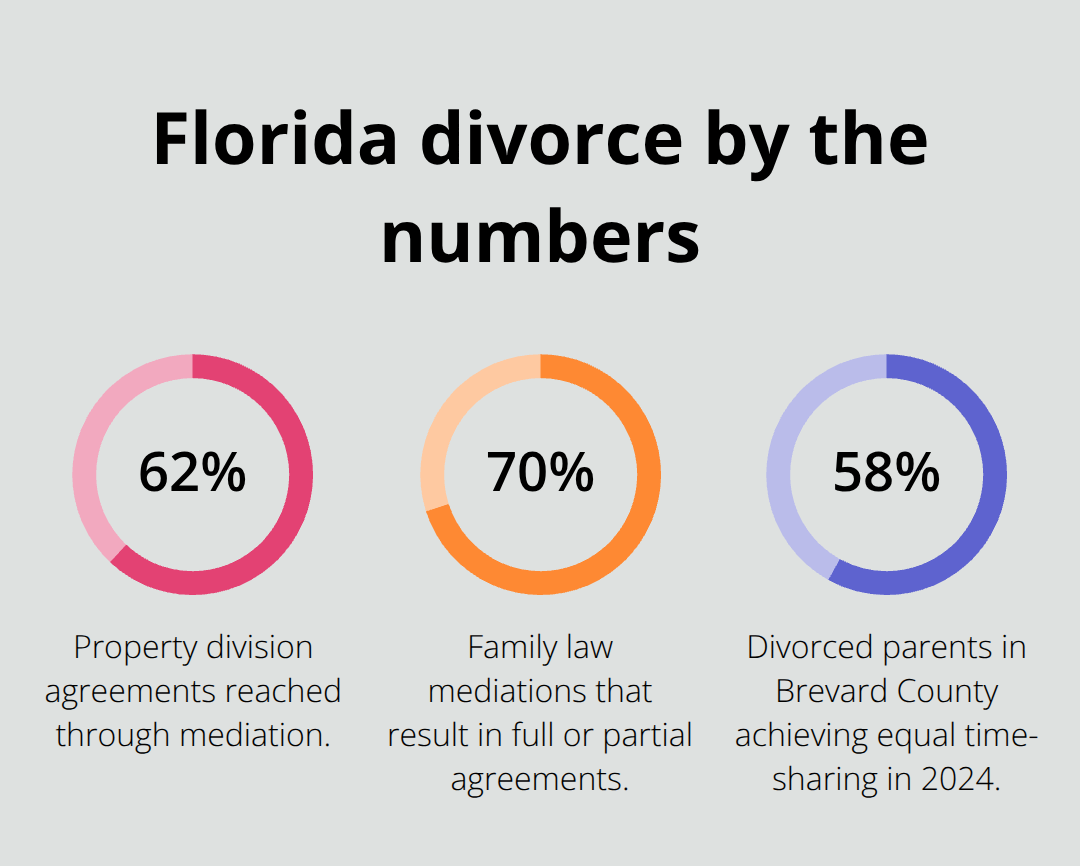

Florida’s equitable distribution law doesn’t mean equal. Section 61.075 of the Florida Statutes sets the framework, but what actually matters is whether your settlement reflects your specific situation. A fair agreement accounts for how long you were married, what each spouse contributed financially and as a homemaker, interruptions to careers or education, and who acquired or enhanced assets during the marriage. The Florida Bar reports that 62% of divorces reach property division agreements through mediation, which suggests most people find middle ground without trial. However, you shouldn’t settle just because mediation exists. The court considers nine specific factors when dividing marital property, and your settlement should reflect these same considerations.

Understanding Alimony in Your Settlement

If you were married 17 years or longer, courts typically award permanent alimony; if you were married under 10 years, durational or bridge-the-gap alimony becomes more common. According to a 2023 study, durational alimony was awarded in about 45% of alimony cases. Your settlement must account for this reality. Many people undervalue retirement accounts or miss passive appreciation on nonmarital assets that became marital through commingling. Marital property includes assets acquired during marriage and appreciation of nonmarital assets funded by marital money. This distinction matters enormously because it shifts thousands of dollars between spouses.

Identifying Every Asset and Liability

Start by listing real estate, vehicles, retirement accounts, investment accounts, business interests, digital assets like cryptocurrency, and even professional licenses if applicable. Nonmarital assets acquired before marriage or through gifts and bequests from third parties stay nonmarital unless you commingled them or used marital funds to enhance them. Real property held as tenants by the entireties carries a strong presumption of being marital, regardless of when purchased. Debts matter equally: credit card balances, mortgages, car loans, and tax liabilities all factor into equitable distribution. If your spouse pledged nonmarital property as collateral for a marital loan, Florida courts treat this inconsistently case by case, so documentation becomes critical.

Valuing Business Interests and Retirement Benefits

Business valuations require fair market value assessments, and enterprise goodwill developed during marriage becomes a marital asset. Retirement benefits accrued during the marriage are marital assets; the valuation date typically falls on the separation date, filing date, or final hearing date depending on circumstances. You should build a comprehensive inventory with supporting documents: deeds, account statements, retirement plan statements, tax returns, and appraisals for significant assets. Many people forget digital assets or underestimate household items, but a complete list prevents post-divorce disputes and ensures nothing slips through.

How Florida Courts Actually Divide Property

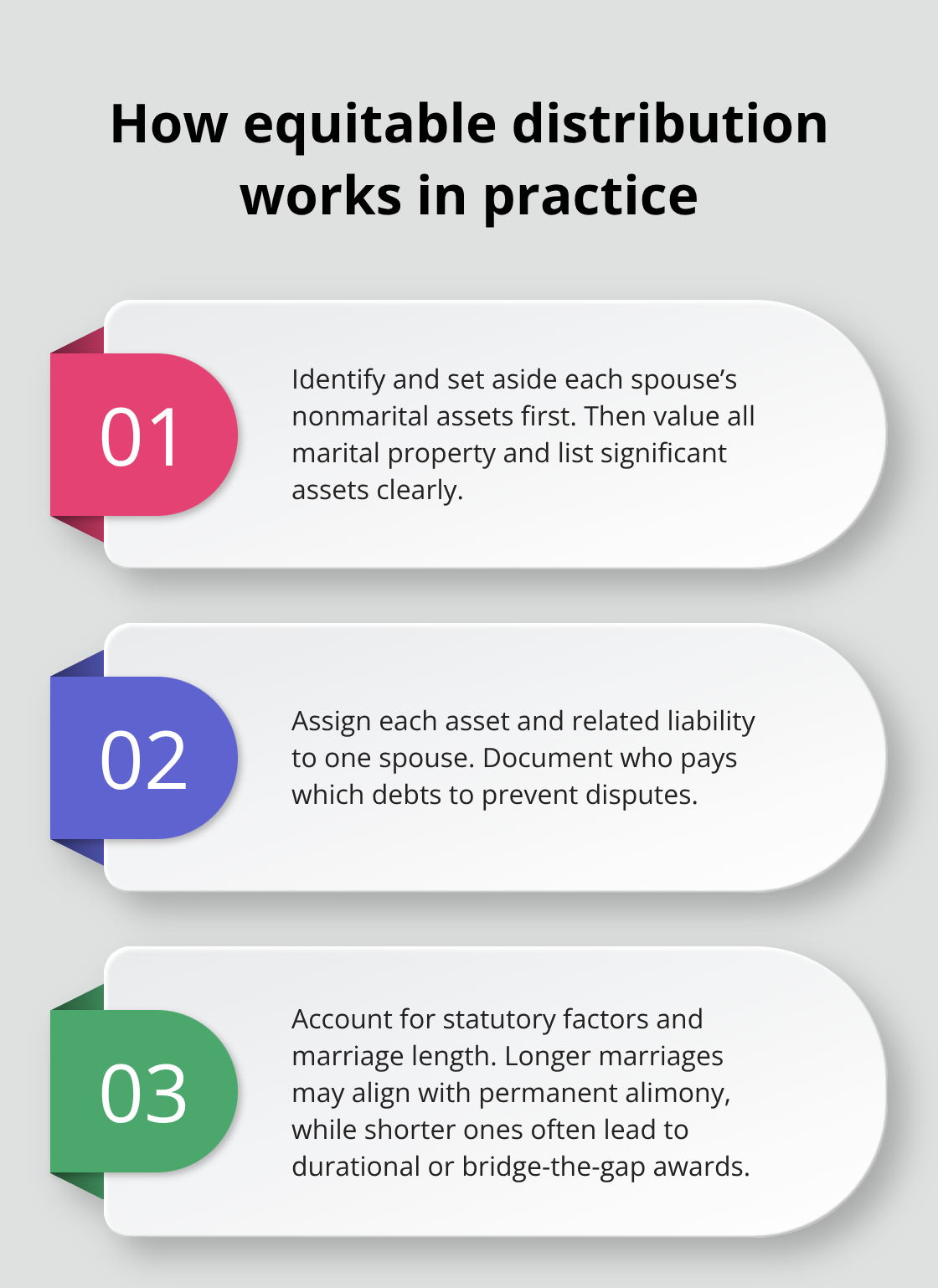

The court starts by setting aside each spouse’s nonmarital assets, then distributes marital property using equitable distribution principles. Equitable doesn’t guarantee 50/50; it means fair under the circumstances. Courts weigh each spouse’s economic situation, earning potential, interruptions to careers or education, and contributions to the other spouse’s professional advancement. If one spouse sacrificed education or career opportunities to raise children or support the other spouse’s education, the court may award unequal distribution to compensate. Intentional dissipation or waste of marital assets within two years before filing can influence distribution against the spouse who wasted funds. The court must issue written findings identifying nonmarital assets, valuing significant assets, and detailing who receives what and who pays which liabilities. This documentation protects both parties because it creates a clear record. Cash awards ordered as part of distribution vest immediately and remain a debt unless parties agree otherwise. The judgment itself functions as a conveyance instrument when recorded in county records, so proper legal drafting matters. Settlement agreements should mirror this same precision: identify each asset, state its value, assign it to one spouse, and address liabilities clearly. Once you understand how courts divide property and what factors influence alimony, you can move forward with negotiation strategies that protect your interests.

Negotiating Without Leaving Money on the Table

Know Your Walk-Away Point Before Negotiations Start

Settlement negotiations fail when one spouse enters discussions without a clear strategy. You need to know your walk-away point before you sit down to talk, and you need documentation to back up every claim about asset value and income. Start by ranking your priorities into three tiers: items you will not compromise on, items worth trading, and items you can concede. Most people fight hardest over emotional issues rather than financial ones. If keeping the family home matters more to you than retirement accounts, state this explicitly to your attorney. Courts in Brevard County reported that 58% of divorced parents achieved equal time-sharing arrangements in 2024, which tells you something important: judges prefer balanced outcomes when parents cooperate. If you fight over every dollar, you signal to the court that you cannot cooperate, which undermines your credibility in custody disputes.

Use Data to Strengthen Your Position

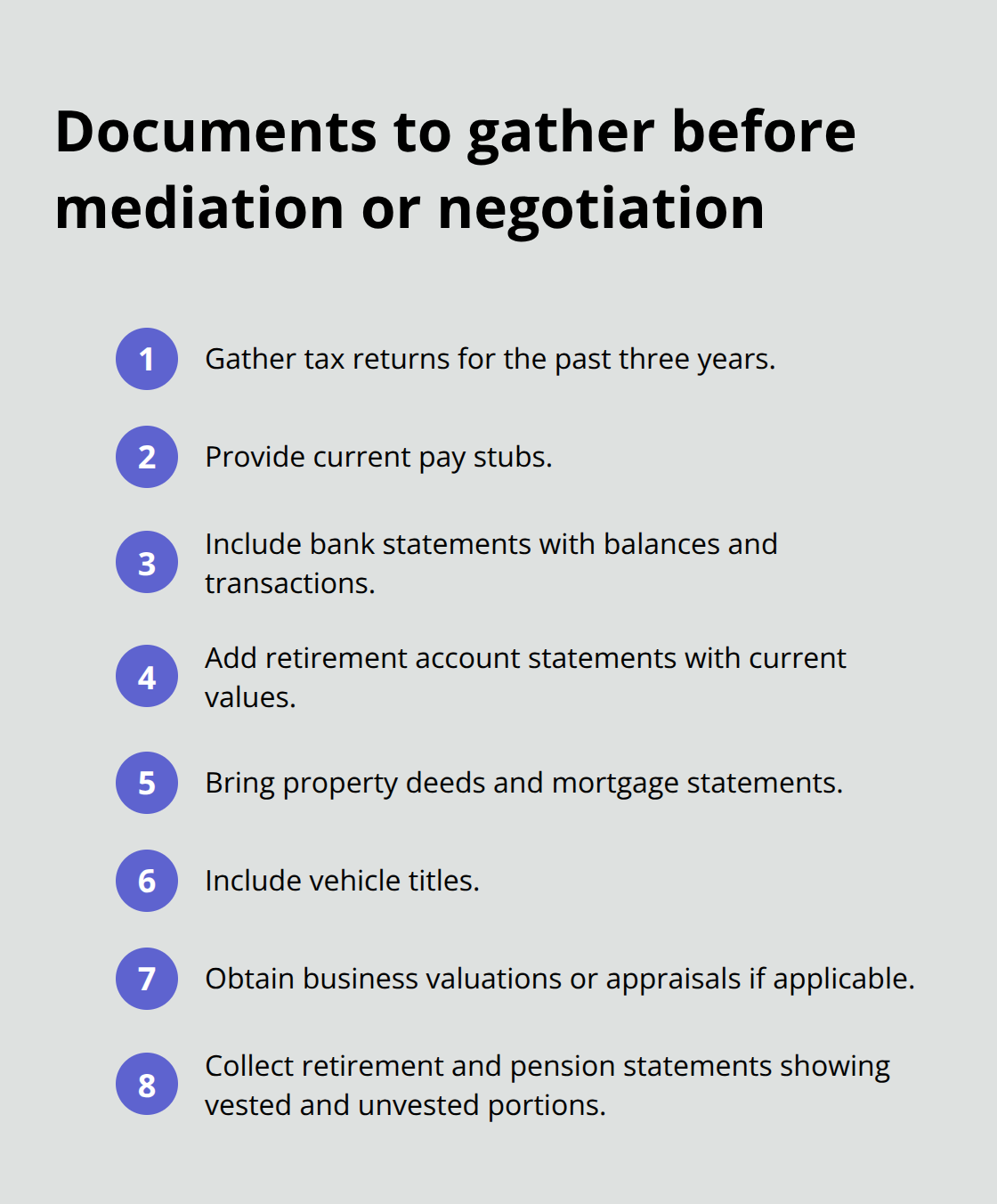

The Florida Dispute Resolution Center found that roughly 70% of family law mediations result in full or partial agreements, meaning most cases settle when both sides engage honestly. This statistic should influence your approach: settlement is statistically more likely than trial, so positioning yourself as reasonable strengthens your negotiating power. Bring your attorney complete financial documentation from day one. Tax returns for the past three years, current pay stubs, bank statements showing account balances and transaction history, retirement account statements with current values, property deeds and mortgage statements, and vehicle titles all become ammunition in negotiations.

If your spouse claims an asset is worth less than it actually is, you need documentation to prove otherwise. Business valuations require appraisals or fair market value assessments; retirement benefits need current statements showing vested and unvested portions. Without this documentation, you cannot negotiate effectively because you cannot verify claims.

Avoid Common Settlement Mistakes

Many people sabotage their own settlements by making emotional decisions or accepting the first offer. An attorney familiar with Brevard County divorce patterns can tell you whether a proposed alimony amount aligns with what courts actually award for your marriage length and income situation. Durational alimony was awarded in about 45% of alimony cases according to a 2023 study, yet people routinely accept permanent alimony offers they do not deserve or reject reasonable durational offers out of anger. Your attorney should model different settlement scenarios showing you the after-tax impact of each option, because a lump-sum asset distribution and ongoing alimony have very different long-term consequences.

One common mistake involves undervaluing retirement accounts or pension plans. Courts value these at the separation date or filing date without post-dissolution contributions, and if your spouse has a pension, the present value calculation can shift thousands of dollars. Another frequent error occurs when people agree to keep the marital home without adjusting other asset divisions to account for the home’s equity. If the home is worth $400,000 with a $200,000 mortgage, you accept $200,000 in equity while your spouse receives other assets of lesser value, and you remain stuck with ongoing property taxes, insurance, and maintenance costs. Settlement agreements should address this imbalance explicitly.

Get Legal Review Before You Sign

We at Harnage Law PLLC recommend that clients avoid signing anything without having an attorney review it first, because once you sign, modifying that agreement becomes extremely difficult. Courts presume settlement agreements are fair if both parties had legal representation, so the decision to forego an attorney can cost you tens of thousands of dollars in unfavorable terms that cannot be undone. With your priorities ranked, documentation gathered, and common pitfalls identified, you now understand how to approach negotiations strategically. The next step involves learning how courts actually calculate alimony and support obligations, and how to structure your settlement to protect your financial future.

Property Division and Alimony in Your Settlement

How Florida Courts Divide Marital Property

Florida courts divide marital property using equitable distribution, which means fair but not necessarily equal. The court’s process follows a strict sequence: identify and set aside each spouse’s nonmarital assets first, then value all marital property, assign each asset to one spouse, and address liabilities. Courts consider nine specific factors when deciding how to split assets, and your settlement agreement should reflect this same analysis. The marriage duration heavily influences outcomes.

Marriages over 17 years typically result in permanent alimony awards, while marriages under 10 years usually trigger durational or bridge-the-gap alimony instead.

Understanding Alimony Awards and Duration

A 2023 study found durational alimony was awarded in about 45% of alimony cases, yet many people accept permanent alimony offers they do not deserve simply because they lack knowledge about what courts actually award. Your settlement must account for how courts value retirement benefits, which are assessed at the separation date, filing date, or final hearing date without including post-dissolution contributions. Pension plans require present value calculations that can shift thousands of dollars between spouses. Business interests receive fair market value assessments, and any enterprise goodwill developed during the marriage becomes marital property subject to division.

Protecting Nonmarital Assets in Your Agreement

Real property held as tenants by the entireties carries a strong presumption of being marital regardless of when purchased, which means you cannot claim it as nonmarital property without clear documentation proving otherwise. Intentional dissipation or waste of marital assets within two years before filing can influence the court against the spouse who wasted funds, so if your spouse depleted accounts or transferred assets improperly, document this thoroughly before settling.

Structuring Your Settlement for Long-Term Financial Security

Many people accept the marital home without adjusting other asset divisions to compensate for ongoing property taxes, insurance, maintenance, and potential mortgage obligations. If the home has $400,000 in value with a $200,000 mortgage, you receive $200,000 in equity but carry ongoing expenses your spouse avoids. Your settlement should address this imbalance explicitly by assigning additional assets to the spouse keeping the home or reducing their alimony obligation.

Lump-sum distributions and ongoing alimony create vastly different financial pictures after taxes. A settlement offering $150,000 in assets plus $1,500 monthly alimony for five years totals $240,000 over that period, but the alimony portion is taxable income while the lump-sum asset distribution is not. An attorney can model multiple settlement scenarios showing the after-tax impact of each option, which prevents you from accepting seemingly attractive offers that prove financially damaging long-term.

Cooperation and Credibility in Negotiations

Courts prefer balanced outcomes when spouses agree on major issues like property division and alimony, which demonstrates that judges value cooperation in settlement negotiations. Positioning yourself as reasonable strengthens your credibility in custody disputes and signals to the court that you prioritize your children’s stability over financial warfare.

Final Thoughts

A divorce settlement in Melbourne, Florida succeeds when both spouses understand what they are trading and why. The process requires honest assessment of your priorities, complete financial documentation, and realistic expectations about what courts actually award. You now know how Florida’s equitable distribution laws work, what factors judges consider, and how to avoid common mistakes that cost thousands of dollars.

Concrete action moves you forward immediately. Gather your financial documents now: tax returns, pay stubs, bank statements, retirement account statements, and property deeds. Rank your priorities into three tiers so you know what you will fight for and what you can concede. Document every asset and liability, including digital assets and business interests, because this documentation strengthens your negotiating position significantly.

We at Harnage Law PLLC provide personalized attention and strategic counsel to help you navigate these decisions with confidence. Our team understands the local court system and can model different settlement scenarios showing you the after-tax impact of each option, which prevents you from accepting offers that seem attractive but prove financially damaging long-term. Contact us to discuss your divorce settlement and learn how we can help you achieve the best possible outcome.