How to Handle Divorce Settlements: A Practical Approach

Our Blog

How to Handle Divorce Settlements: A Practical Approach

Divorce settlements in Melbourne, Florida involve complex decisions about assets, finances, and your future. Getting these decisions right matters because mistakes can cost you thousands of dollars and years of regret.

We at Harnage Law PLLC help people handle divorce settlements by breaking down the process into manageable steps. This guide walks you through what actually happens during settlement negotiations and how to avoid the pitfalls that catch most people off guard.

What Actually Gets Divided in Your Settlement

Florida law requires courts to divide marital assets and liabilities between spouses, but the process isn’t as straightforward as splitting everything 50/50. The state follows equitable distribution, meaning the court aims for fairness rather than an automatic equal split. This matters because it gives you leverage in negotiations if you understand what counts as marital property and what stays off the table.

Marital assets include anything acquired during the marriage, retirement accounts earned during those years, real estate held as tenants by the entireties, and even the increase in value of nonmarital property if marital effort or funds caused that increase. Nonmarital assets-property owned before marriage, inheritances, and gifts received individually-generally remain yours alone. The problem most people face is that they don’t document what’s nonmarital early enough. If you inherited money and deposited it into a joint account, you’ve likely lost your claim to it being separate property unless you can trace it clearly through financial records. The law places the burden on you to prove nonmarital status with clear and convincing evidence, not the other way around.

Timing Matters for Asset Classification

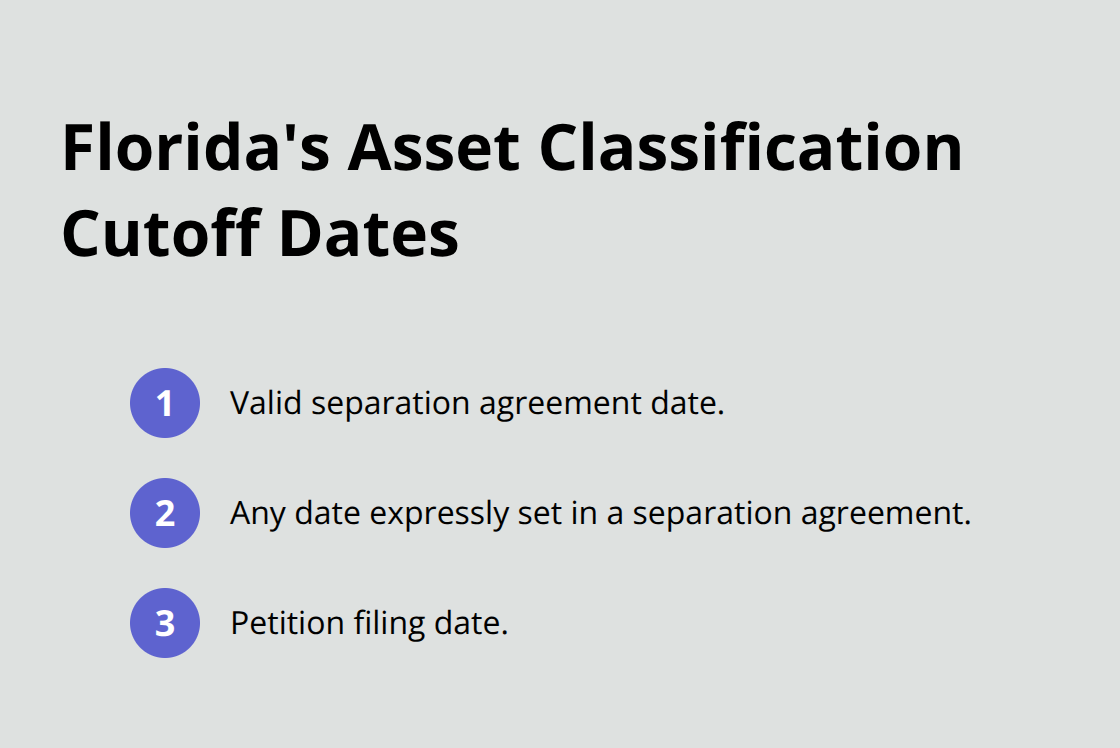

The classification cutoff date determines whether an asset counts as marital or nonmarital. Florida law uses the earliest of three dates: a valid separation agreement date, any date expressly set in a separation agreement, or the petition filing date. This means assets acquired after you file for divorce are presumed marital unless you prove otherwise.

If you wait to file because you think it helps your position, understand that every day you delay adds more assets to the marital pool.

Real property valuation dates can vary by asset type-some are valued at separation, others at the final hearing if they appreciated due to marital effort. Professional goodwill, business assets, and retirement accounts require specific valuation methods. A lump-sum cash award in a settlement vests immediately at judgment and becomes a debt owed unless both parties agree otherwise. This is why the settlement language matters tremendously.

Nonmarital Property Isn’t Always Protected

Many people assume inheritances and gifts stay separate, but Florida courts have ruled repeatedly that commingling nonmarital funds into marital accounts converts them into marital property. If you received a $100,000 inheritance and deposited it into the joint checking account, that money is now marital property subject to division. Active appreciation of nonmarital real estate due to marital efforts also becomes marital.

Passive appreciation-the property increasing in value simply because the market improved-stays nonmarital. The distinction matters enormously, and courts use a coverture fraction calculation to determine the marital portion of appreciation. If you used marital funds to pay down a mortgage on property you owned before marriage, that mortgage principal paid becomes marital property owed to your spouse.

How Commingling Changes Everything

Commingling nonmarital funds into joint accounts is one of the fastest ways to lose protection of separate property. Once you mix inheritance money, gifts, or pre-marriage savings with marital accounts, courts treat the entire balance as marital unless you can trace the separate funds through detailed financial records. This traceability requirement (proving exactly where the money came from and where it went) falls on you, not your spouse. Documentation matters far more than your word alone.

Understanding these rules now gives you time to gather documentation proving what’s truly separate, and it helps you negotiate from a position of knowledge rather than assumption. The next section covers how to actually negotiate these asset divisions and what trade-offs typically occur when settlements are structured.

Structuring Deals That Actually Work

Settlement negotiations in Melbourne, Florida revolve around three core elements: property division, support obligations, and parenting arrangements if children are involved. Most people approach settlements thinking they need to win on every front, but experienced negotiators understand that successful settlements involve strategic trade-offs. If you care deeply about keeping the family home, you might accept a smaller share of retirement accounts. If maintaining primary custody matters most, you could agree to higher child support or alimony. The key is identifying what actually matters to your future versus what you’re willing to concede. Florida law requires financial disclosures from both parties within a specified timeframe, and mediation is mandatory in most cases unless domestic violence is present. This mandatory mediation process forces both sides to negotiate seriously rather than posture, which typically leads to faster resolutions than contested trials.

Valuation Errors That Cost Thousands

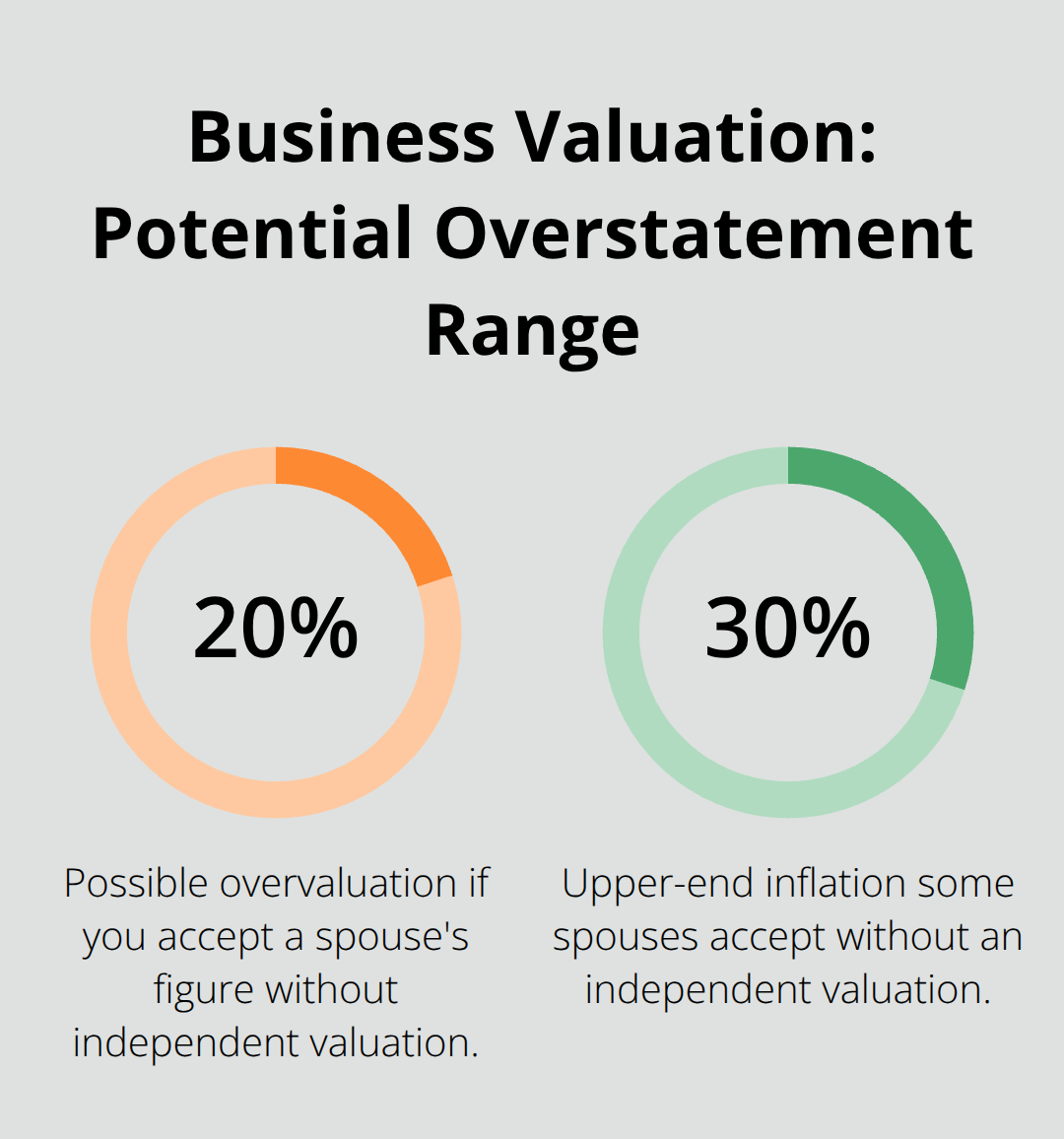

Asset valuations drive settlement outcomes more than any other factor. If your spouse’s business is valued at $500,000 and you accept that figure without independent valuation, you might be accepting a number that’s 20 to 30 percent inflated. Professional goodwill valuations require a fair market value approach, which means calculating what a willing buyer would pay minus the tangible business assets.

Retirement accounts must be valued as of the dissolution date, not projected values decades into the future. If your spouse claims they’ll take early retirement to reduce the account’s present value, Florida courts have ruled that early retirement penalties shouldn’t reduce your marital share. Real estate valuations matter equally-appraisals from six months ago don’t reflect current market conditions. Insist on current appraisals dated within 30 days of your settlement discussions.

Tax Consequences You Cannot Ignore

Tax implications of asset transfers get overlooked constantly. When you transfer investment property to your spouse as part of settlement, you avoid federal capital gains taxes on that transfer itself. However, if your spouse later sells that property, capital gains taxes apply based on the original purchase price. This means accepting an investment property worth $300,000 today might cost you more in future taxes than accepting equivalent cash. The Tax Cuts and Jobs Act changed alimony tax treatment in 2018, making alimony non-deductible for the payer and non-taxable income for the recipient in divorces finalized after December 31, 2018. This fundamentally changed settlement math because higher alimony payments no longer provide tax deductions to the paying spouse.

Deciding Whether to Accept or Reject Offers

The decision to accept or reject a settlement offer depends on comparing the offer’s value to your likely outcome at trial. If your spouse offers you 45 percent of marital assets and you believe a judge would award you 50 percent, the math seems simple-reject it. But trials cost money. A contested divorce trial in Florida can cost $15,000 to $50,000 in attorney fees depending on complexity, and the process takes months. If the additional 5 percent of assets you might win equals $30,000, but trial costs eat up $25,000 in fees, your net gain shrinks to $5,000. Factor in the emotional cost, the uncertainty of trial outcomes, and the time investment required. Most people underestimate how unpredictable judges can be on certain issues. Child custody decisions, for example, turn on best-interest-of-the-child factors that vary significantly by judge. A settlement offer guaranteeing you 55 percent parenting time might be more valuable than rolling the dice on trial hoping for 60 percent.

Precise Language Protects Your Future

Documentation of your settlement agreement must be precise and thorough. Vague language about property division creates post-judgment disputes that cost thousands to litigate. Instead of writing that you’ll receive your retirement account, specify the exact account number, current balance, and the portion you’re receiving. If your spouse keeps the marital home, the settlement should detail who pays the mortgage, property taxes, insurance, and homeowners association fees during the period before the deed transfers. The judgment distributing real property functions as a conveyance when recorded in the county where the property is located, but recordation is essential-without it, title issues can plague you for years. Lump-sum cash awards vest immediately at judgment and become a debt owed, while periodic payments require enforcement mechanisms if the paying spouse defaults. Have your attorney review all settlement language before you sign anything, because corrections become exponentially harder after judgment is entered.

The specificity you build into your settlement agreement now determines whether enforcement runs smoothly or whether you’ll face costly disputes later. With your settlement structure in place, the next step involves understanding what mistakes derail even well-negotiated agreements and how to avoid them.

Avoiding Costly Mistakes During Settlement

Hidden assets destroy more settlements than any other factor. Florida law requires both parties to provide complete financial disclosures within a specified timeframe before mediation occurs, yet people routinely omit accounts, investments, or income streams. If your spouse owns a second property in another state, that asset must be disclosed. If they have cryptocurrency holdings, business interests, or cash savings accounts you don’t know about, those count too. The problem isn’t that people forget-it’s that they deliberately hide assets thinking they won’t get caught.

Courts in Melbourne, Florida impose severe penalties for asset concealment, including awarding the undisclosed amount entirely to the other spouse plus attorney fees and sanctions. A spouse who hides $150,000 in a hidden bank account doesn’t just lose that $150,000 to you; they often face additional penalties that make the total cost $200,000 or more. Before you sign any settlement, demand complete bank statements for the past two years, brokerage account statements, business tax returns, and retirement account statements dated within 30 days. If your spouse claims they have no other assets, require them to sign an affidavit under oath stating that. This creates legal liability if they later admit to hidden accounts.

Tax Treatment Reshapes Settlement Value

Tax consequences of settlement terms create financial damage that unfolds over years. Alimony payments are no longer tax-deductible for the payer under the Tax Cuts and Jobs Act for divorces finalized after December 31, 2018, which means the paying spouse loses deduction value but the receiving spouse doesn’t owe income tax on it. This fundamentally changed settlement math-a spouse paying $3,000 monthly in alimony gets no tax benefit, while in pre-2019 divorces that same payment reduced their taxable income by $36,000 annually.

Property transfers within divorce avoid federal capital gains taxes on the transfer itself, but your spouse could sell that property later and trigger capital gains taxes based on the original purchase price. If you accept a rental property valued at $400,000 today but your spouse originally paid $250,000, your spouse avoids $150,000 in capital gains tax exposure while you inherit it. Investment accounts with significant unrealized gains require valuation with after-tax impact calculated. A brokerage account showing $300,000 in gains might be worth 25 percent less after taxes if liquidated.

Retirement accounts split through a Qualified Domestic Relations Order avoid immediate taxes, but withdrawals in retirement will be taxed as ordinary income. Rushing through settlement without having a tax professional review the numbers costs thousands in overlooked tax consequences. Before you accept any settlement, have a CPA or tax advisor model the tax impact of each asset you’re receiving and each payment obligation you’re accepting.

Vague Language Creates Post-Judgment Disputes

Signing a settlement without legal review ranks as the costliest mistake people make in Melbourne, Florida divorce cases. Settlement agreements involve language precision that determines enforceability for years. Vague terms about asset transfer create post-judgment disputes requiring expensive litigation to resolve. If your settlement states that your spouse will transfer their interest in the marital home but doesn’t specify a timeline, your spouse could delay transfer indefinitely while you’re stuck paying the mortgage.

If a lump-sum cash award doesn’t specify payment timing or consequences for default, collecting that money becomes a protracted legal battle. Many people accept settlements thinking they can renegotiate terms later if they change their mind-this is false. Once a judge enters a final judgment, modifying that judgment requires showing a substantial change in circumstances, which is a much higher legal bar than simply deciding you made a bad deal.

The time to negotiate precise language is before you sign, not after. Have an attorney review every settlement agreement, including the specific account numbers for asset transfers, the exact payment amounts and due dates, the recorded property descriptions for real estate transfers, and the enforcement mechanisms if your spouse fails to comply. This review typically costs $500 to $1,500 and prevents $25,000 to $100,000 in future problems. The cost of that review is negligible compared to the cost of enforcing a poorly drafted agreement or discovering later that you accepted terms far worse than what a judge would have ordered.

Final Thoughts

Successful divorce settlements in Melbourne, Florida rest on three foundational principles: understanding what assets count as marital property, negotiating from a position of knowledge rather than emotion, and refusing to sign anything without legal review. The mistakes that cost people the most money happen before settlement agreements are finalized, not after. Hidden assets, overlooked tax consequences, and vague settlement language create financial damage that compounds for years.

The decision to handle how to handle divorce settlements alone versus with legal representation comes down to complexity and risk tolerance. If your divorce involves only modest assets, no children, and both parties agree on division, you might navigate the process without an attorney. Most divorces in Melbourne, Florida involve complications that make legal representation invaluable, and we at Harnage Law PLLC provide experienced legal guidance for family law cases including divorce and child custody.

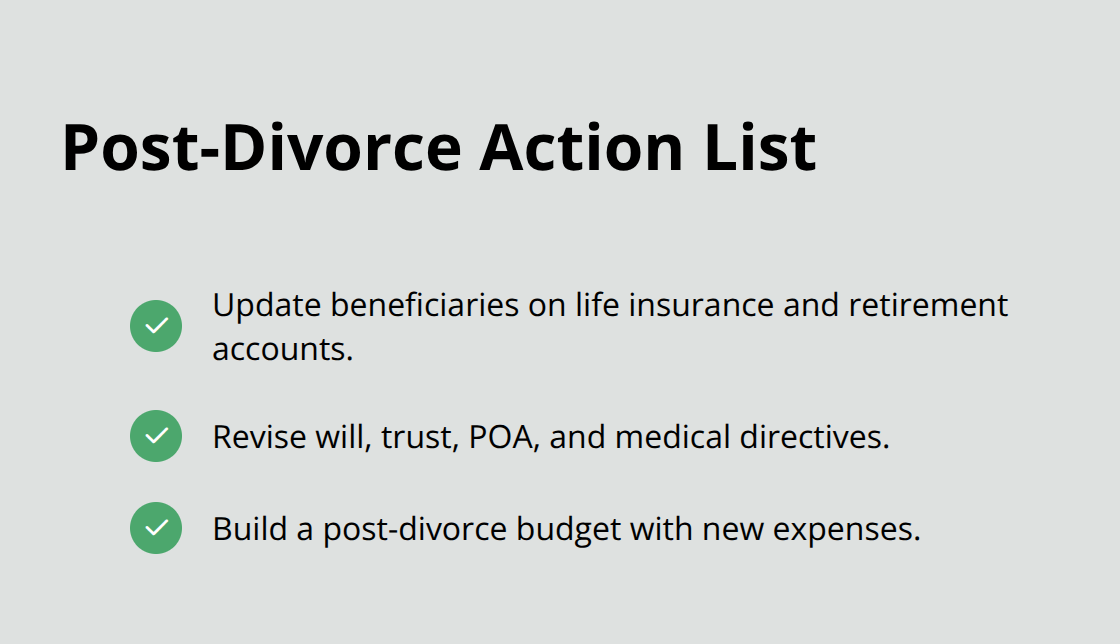

After your settlement becomes final, update your beneficiaries on life insurance policies and retirement accounts immediately, removing your ex-spouse and naming new beneficiaries. Update your will, trust, power of attorney, and medical directives with an estate planning attorney to reflect your new circumstances. Create a post-divorce budget accounting for new expenses like separate housing, updated insurance costs, and any support obligations you now carry.